Canadian real estate leverage has been an increasing concern, and it it’s growing. Filings from Office of the Superintendent of Financial Institutions (OSFI), the federal regulator for banks, show that loans secured by real estate showed huge growth in September. In fact, these loans are now at a record high, and are printing record growth.

Total Loans Secured By Real Estate Now Over $279 Billion

The total of loans secured against residential real estate for business and non business purposes is booming in 2017. Analysis of OSFI data shows $279.64 billion in loans in September, up $25.4 billion from the same month last year. That’s 9.92% growth, which is just off the peak of 12.10% established in June 2017. This year is the first year to see growth above 5%, in the 5 years of filings OSFI provided. The huge growth represents a significant increase, but some of these loans are being used for productive purposes. Let’s break it down.

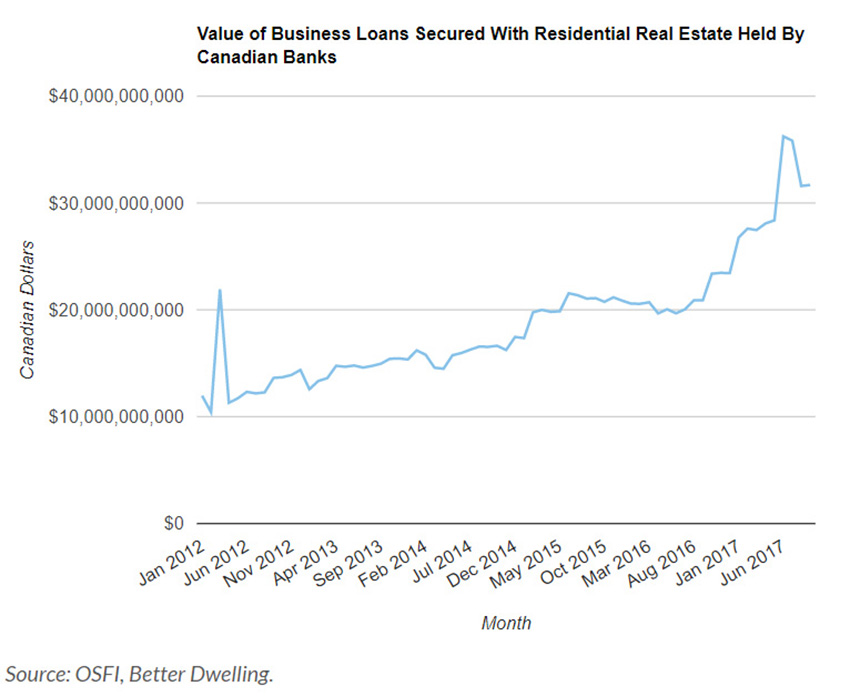

Over 51% Growth For Business Loans Against Residential Real Estate

When people say “good debt,” this is the kind of debt they are typically referring to – borrowing for business. In September, banks held $31.68 billion of loans for business purposes, secured by residential real estate. That’s a massive 51.58% growth from the year before, which is just off peak growth established earlier this year. While the growth is huge, it is just a fraction of the total debt here.

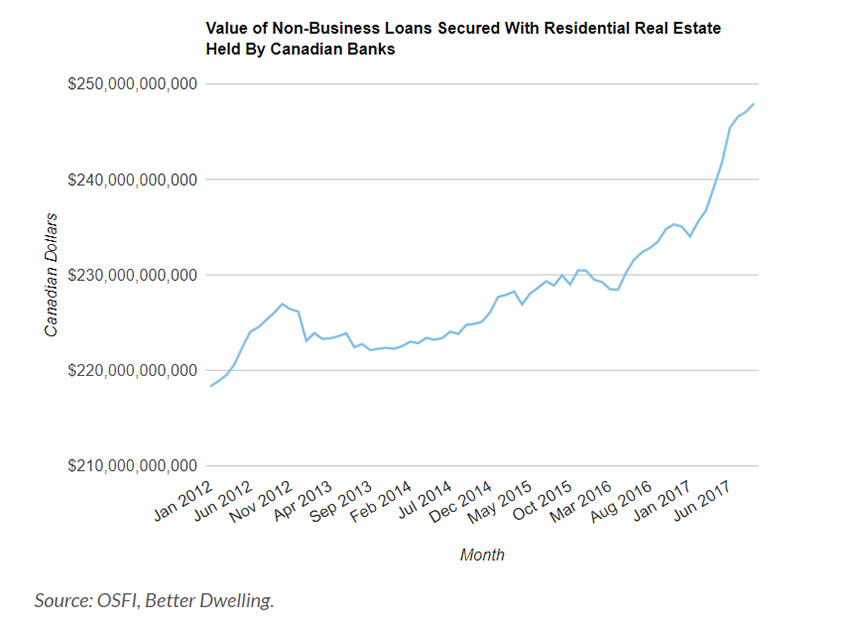

Over $248 Billion Of Personal Loans Secured By Residential Real Estate

Personal loans secured by real estate are experiencing record growth. These are the loans that we have no idea what they did with the money. These can be anything from renovation financing, to buying second homes, or even possibly using home equity to buy bitcoin – no one’s quite sure. At the end of September, banks held $248.95 billion in personal loans secured by residential real estate, a 6.91% increase from last year. This is the highest annual growth observed in the OSFI filings.

OSFI filings only include federally regulated banks, so credit unions and private lenders aren’t included in these numbers. This means there’s likely even more debt secured against real estate. This leverage is relatively harmless when things are good, but has the potential to be an issue in the event of a home price correction. Especially if that correction means a recession.