A sudden sharp rise in interest rates that could cause Canadian home prices to plunge 30 per cent would trigger more than $1-billion in losses to the country's government-backed mortgage insurer, according to the results of stress tests released today by the federal housing agency.

Canada Mortgage and Housing Corp. released the results of internal modelling that show how vulnerable its mortgage insurance and securitization business is to a variety of severe economic shocks. The agency, which began publishing its stress tests last year, described the process as "searching out extreme scenarios that have a very remote chance of happening and planning for them."

CMHC tested its portfolios against several different hypothetical scenarios. The events are not forecasts, but a test of how likely the taxpayer-backed institution would be to withstand a series of doomsday-style economic surprises without needing a government bailout.

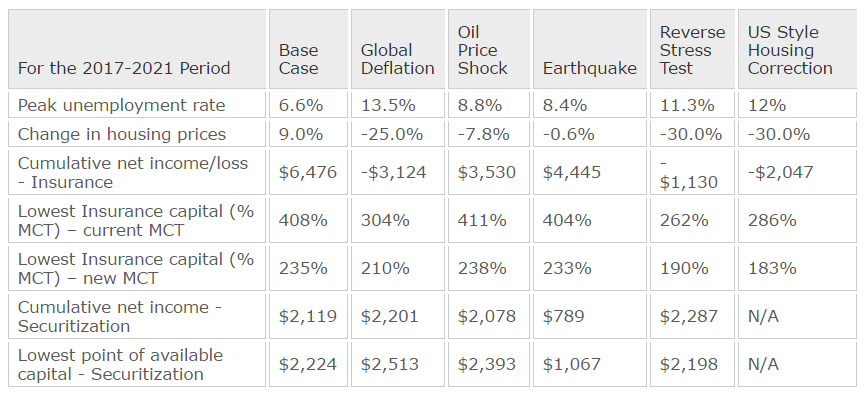

It studied how its portfolio would perform if interest rates suddenly rose by 2.4-percentage points over two quarters, triggering a home-price crash, a rise in the unemployment rate to 11.3 per cent and the failure of a Canadian lender. CMHC's insurance business would lose $1.13-billion in that case.

Despite the prospect of steep losses in its insurance business in the wake of a sever and unexpected economic shock, the federal agency said the results of its stress testing show that it holds enough capital to keep operating, even under dire circumstances.

The Office of the Superintendent of Financial Institutions, the federal financial regulator, sets the minimum amount of capital that lenders and insurers are require to hold to withstand a severe hit to their business. Insurance companies such as CMHC are required to stop writing new insurance business if their capital ratio falls below 100 per cent of required minimum level set by OSFI. They become insolvent if their capital levels hit zero.

CMHC's stress tests show it would suffer the most dramatic losses in the event of a severe and prolonged global economic depression that sent unemployment soaring to 13.5 per cent and triggered a 25-per-cent drop in national home prices. In that case CMHC said its mortgage insurance business could lose more than $3.1-billion over five years. However CMHC said it would have more than 200 per cent of its required minimum capital, even after accounting for stricter capital requirements that OSFI is expected to introduce in January.

CMHC's stress testing comes amid heightened concerns over the health of the Canadian housing market. Last month, the housing agency issued its first "red" warning for Canada's housing market as a whole, saying it now sees "strong evidence of problematic conditions" in six of the country's largest housing markets.

In yet another scenario the Crown corporation said its insurance business would lose more than $2-billion if Canada experienced a "U.S.-style" housing correction, where home prices drop by 30 per cent and the unemployment rate rises to 12 per cent.

The insurer predicted it would still stand to turn a profit even if oil prices fell to $20 (U.S.) a barrel next year and remained between $20-30 for the next four years, a scenario that involved the national unemployment rate rising to 8.8 per cent and home prices dropping by 7.8 per cent. (West Texas Intermediate crude has hovered between $40-$50 a barrel for much of the past year.)

CMHC also tested its business against the prospect of a high-magnitude earthquake that delivered critical damage to a major urban centre. The agency would still return a profit to the federal government in that case, which CMHC predicts would cause unemployment to rise to 8.4 per cent and trigger a small decline in national home prices.

The agency said its "base case" scenario – the most realistic economic projections that it uses to set its capital levels – is for unemployment to peak at 6.6 per cent and for home prices to rise 9 per cent over the next five years, in which case CMHC's mortgage insurance business would generate more than $6.4-billion (Canadian) in profits.

The Canadian Real Estate Association reported earlier this week that national home sales hit record levels for October last month while the association's 11-city composite benchmark price soared an annualized 14.6 per cent to $579,800.

The results of each scenario on CMHC’s regulatory capital requirements (% MCT) are as follows:

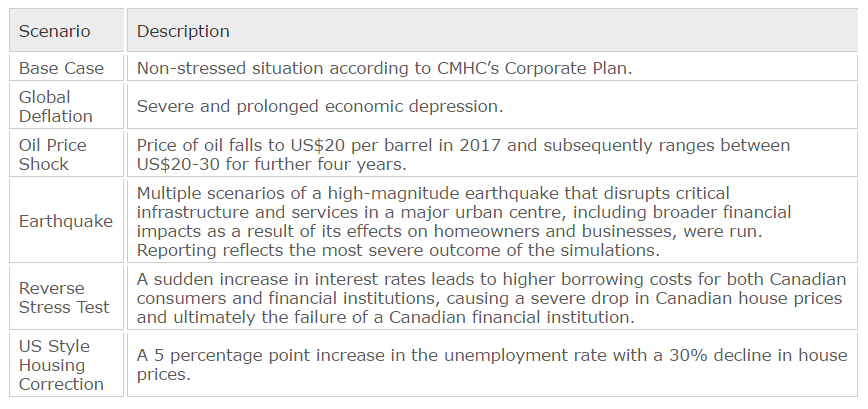

Scenario Descriptions